Does Your Bank Need an Interim Impairment Test Due to the Economic Impact of COVID-19?

Analysts and pundits are debating whether the economic recovery will be shaped like a U, V, W, swoosh, or check mark and how long it may take to fully recover. To find clues, many are following the lead of the healthcare professionals and looking to Asia for economic and market data since these economies experienced the earliest hits and recoveries from the COVID-19 pandemic.Taking a similar approach led me to take a closer look at the Japanese megabanks for clues about how U.S. banks may navigate the COVID-19 crisis. In Japan, the banking industry is grappling with similar issues as U.S. banks, including the need to further cut costs; expanding branch closures; enhancing digital efforts; bracing for a tough year as bankruptcies rise; and looking for acquisitions in faster growing markets.Another similarity is impairment charges. Two of the three Japanese megabanks recently reported impairment charges. Mitsubishi UFJ Financial Group (MUFG) reported a ¥343 billion impairment charge related to two Indonesian and Thai lenders that MUFG owned controlling interests in and whose share price had dropped ~50% since acquisition. Mizuho Financial Group incurred a ¥39 billion impairment charge.In the years since the Global Financial Crisis, there have not been many goodwill impairment charges recognized by U.S. banks. A handful of banks including PacWest (NASDAQ-PACW) and Great Western Bancorp (NYSE-GWB) announced impairment charges with the release of 1Q20 results. Both announced dividend reductions, too.Absent a rebound in bank stocks, more goodwill impairment charges likely will be recognized this year. Bank stocks remain depressed relative to year-end pricing levels despite some improvements in May and early June. For perspective, the S&P 500 Index was down ~5% from year-end 2019 through May 31, 2020 compared to a decline of ~32% for the SNL Small Cap Bank Index and ~34% for the SNL Bank Index.This sharper decline for banks reflects concerns around net interest margin compression, future credit losses, and loan growth potential. The declines in the public markets mirrored similar declines in M&A activity and several bank transactions that had previously been announced were terminated before closing with COVID-19 impacts often cited as a key factor.Price discovery from the public markets tends to be a leading indicator that impairment charges and/or more robust impairment testing is warranted. The declines in the markets led to multiple compression for most public banks and the majority have been priced at discounts to book value since late March. At May 31, 2020, ~77% of publicly traded community banks (i.e., having assets below $5B) were trading at a discount to their book value with a median of ~83%. Within the cohort of banks trading below book value at May 31, 2020, ~74% were trading below tangible book value.Do I Need an Impairment Test?Goodwill impairment testing is typically performed annually. But the unprecedented events precipitated by the COVID-19 pandemic now raise questions whether an interim goodwill impairment test is warranted.The accounting guidance in ASC 350 prescribes that interim goodwill impairment tests may be necessary in the case of certain “triggering” events. For public companies, perhaps the most easily observable triggering event is a decline in stock price, but other factors may constitute a triggering event. Further, these factors apply to both public and private companies, even those private companies that have previously elected to amortize goodwill under ASU 2017-04.For interim goodwill impairment tests, ASC 350 notes that management should assess relevant events and circumstances that might make it more likely than not that an impairment condition exists. The guidance provides several examples, several of which are relevant for the bank industry including the following:Industry and market considerations such as a deterioration in the environment in which an entity operates or an increased competitive environmentDeclines in market-dependent multiples or metrics (consider in both absolute terms and relative to peers)Overall financial performance such as negative or declining cash flows or a decline in actual or planned revenue or earnings compared with actual and projected results of relevant prior periodsChanges in the carrying amount of assets at the reporting unit including the expectation of selling or disposing certain assetsIf applicable, a sustained decrease in share price (considered both in absolute terms and relative to peers)

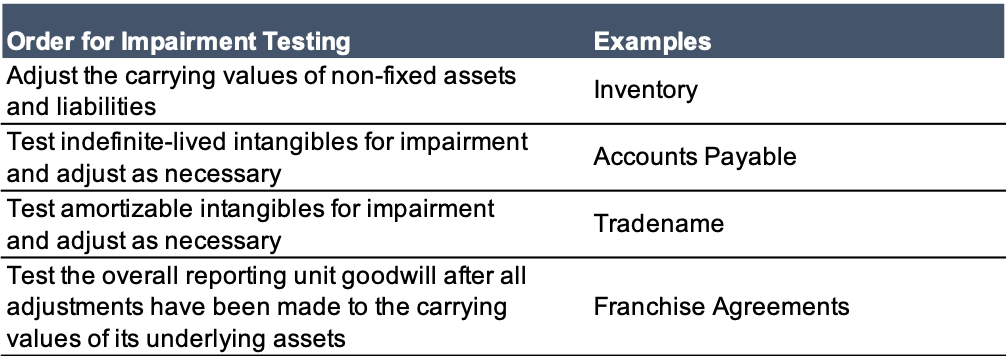

The guidance notes that an entity should also consider positive and mitigating events and circumstances that may affect its conclusion. If a recent impairment test has been performed, the headroom between the recent fair value measurement and carrying amount could also be a factor to consider.How Does an Impairment Test Work?Once an entity determines that an interim impairment test is appropriate, a quantitative “Step 1” impairment test is required. Under Step 1, the entity must measure the fair value of the relevant reporting units (or the entire company if the business is defined as a single reporting unit). The fair value of a reporting unit refers to “the price that would be received to sell the unit as a whole in an orderly transaction between market participants at the measurement date.”For companies that have already adopted ASU 2017-04, the legacy “Step 2” analysis has been eliminated, and the impairment charge is calculated as simply the difference between fair value and carrying amount.ASC 820 provides a framework for measuring fair value which recognizes the three traditional valuation approaches: the income approach, the market approach, and the cost approach. As with most valuation assignments, judgment is required to determine which approach or approaches are most appropriate given the facts and circumstances. In our experience, the income and market approaches are most used in goodwill impairment testing. However, the market approach is somewhat limited in the current environment given the lack of transaction activity in the banking sector post-COVID-19.In the current environment, we offer the following thoughts on some areas that are likely to draw additional scrutiny from auditors and regulators.Are the financial projections used in a discounted cash flow analysis reflective of recent market conditions? What are the model’s sensitivities to changes in key inputs?Given developments in the market, do measures of risk (discount rates) need to be updated?If market multiples from comparable companies are used to support the valuation, are those multiples still applicable and meaningful in the current environment?If precedent M&A transactions are used to support the valuation, are those multiples still relevant in the current environment?If the subject company is public, how does its current market capitalization compare to the indicated fair value of the entity (or sum of the reporting units)? What is the implied control premium and is it reasonable in light of current market conditions?

At a minimum, we anticipate that additional analyses and support will be necessary to address these questions. The documentation from an impairment test at December 31, 2019 might provide a starting point, but the reality is that the economic and market landscape has changed significantly in the first half of 2020.Concluding ThoughtsWhile not all industries have been impacted in the same way from the COVID-19 pandemic and economic shutdown, the banking industry will not escape unscathed given the depressed valuations observed in the public markets. For public and private banks, it can be difficult to ignore the sustained and significant drop in publicly traded bank stock prices and the implications that this might have on fair value and the potential for goodwill impairment.At Mercer Capital, we have experience in implementing both the qualitative and quantitative aspects of interim goodwill impairment testing. To discuss the implications and timing of triggering events, please contact a professional in Mercer Capital’s Financial Institutions Group.Originally published in Bank Watch, June 2020.Request for ProposalMercer Capital is pleased to prepare a proposal for impairment testing services for your bank or bank holding company. Follow the link below to complete a submission.Bank Impairment Testing Proposal Request »